Readings: Valuation and Sustainability

3. Raising Pressure from Investors

The pressure to pursue such a two-pronged valuation and reporting approach is growing. Especially institutional investors (e.g., pension funds or mutual funds) increasingly demand systematic, high-quality information about the firm's non-financial performance.

Most Institutional Investors Consider ESG Factors

For example, a 2018 Survey conducted by EY reports that the overwhelming majority of all surveyed institutional investors conduct a review of a target company's non-financial disclosure related to environmental, social, and governance (ESG) factors. Only 3% of the respondents do not conduct such a review:

The Reporting Quality is Generally Good

The same survey concludes that investors generally believe that most of their target companies provide an adequate assessment of ESG materiality:

Not surprisingly, reporting quality is best with respect to governance factors, as most stock exchanges require firms to provide detailed information about their governance structures. In contrast, there seems to be substantial room for improvement when it comes to social and, especially, environmental factors:

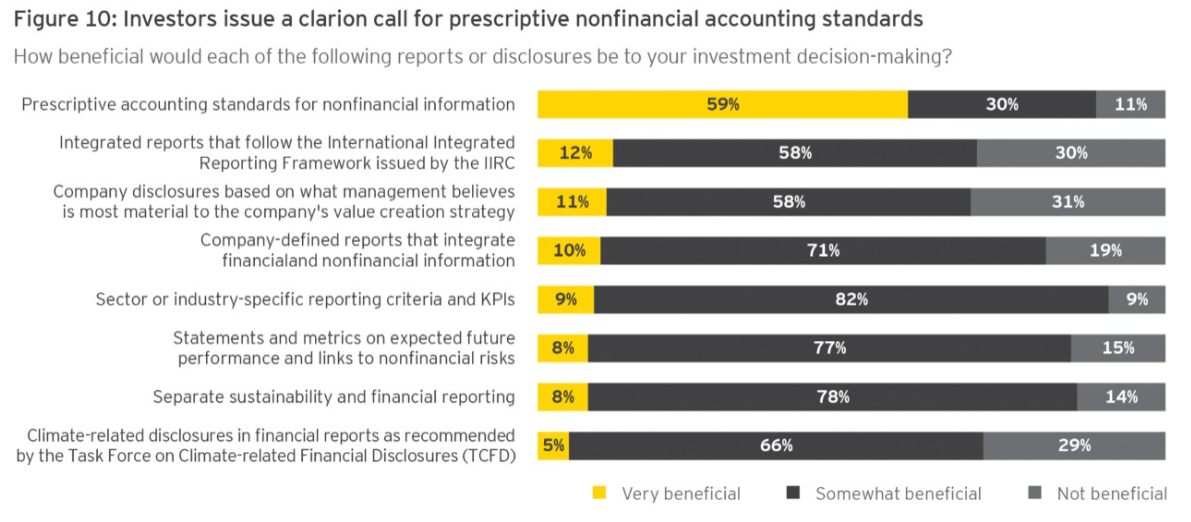

Investors Demand Standardized Information

According to the surveyed investors, information quality could be improved with prescriptive accounting standards for non-financial information, similar to the existing rules in place for material financial information. Investors consider such standardized information more beneficial than company or industry specific disclosures.

And they Rely on National Regulators

Finally, and not surprisingly in light of the above preference for prescriptive accounting standards, the surveyed investors believe that national regulators are best suited to close the information gap. International organizations and NGOs also play an important role.