Reading: DCF for Startups

Abschlussbedingungen

Anzeigen

1. Introduction

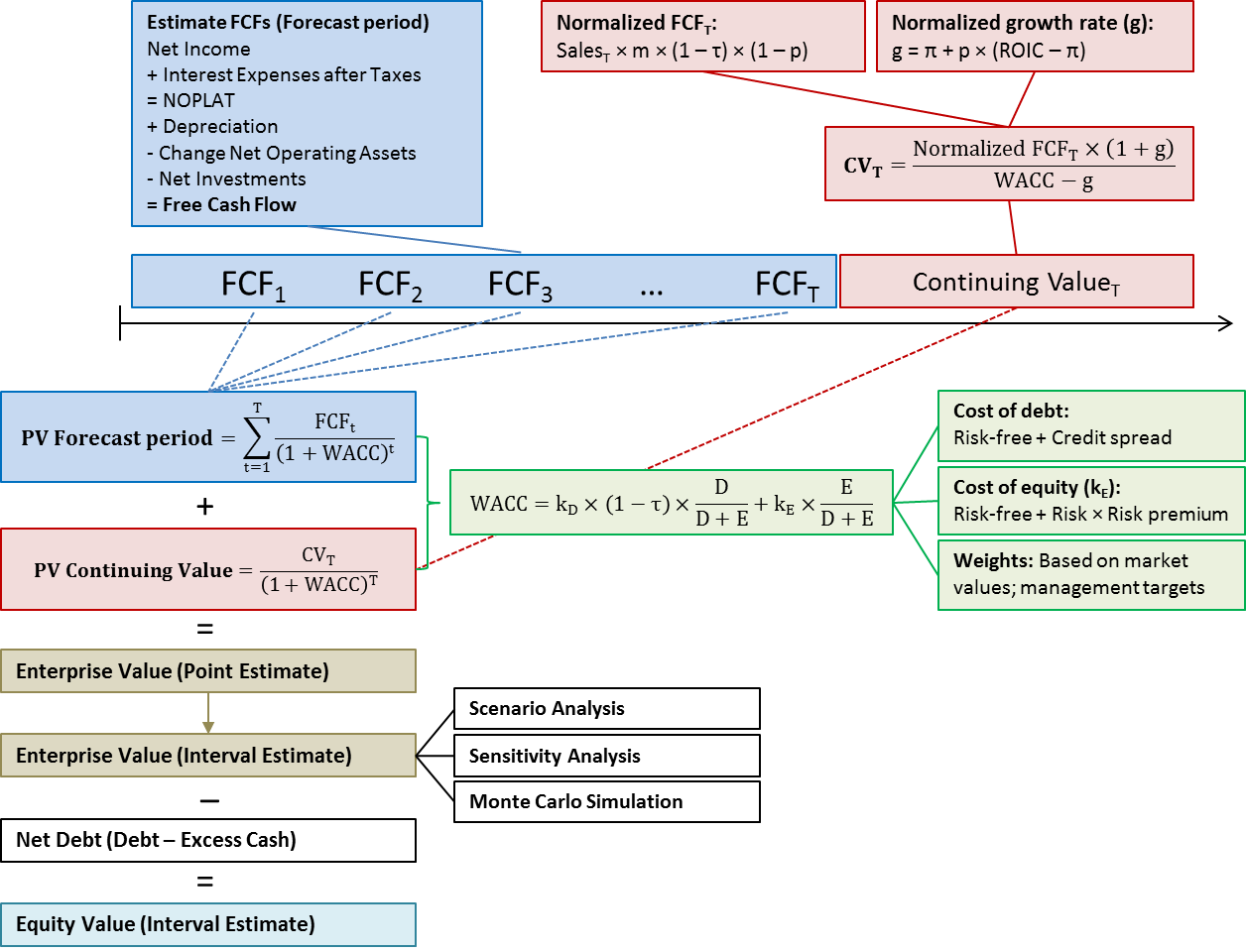

In the course Firm Valuation, we have discussed in great detail how to implement the discounted cash flow approach. We have seen that this valuation method can be roughly summarized by the following graph:

In words, the major steps that bring us from a "blank sheet of paper" to the DCF value of the firm's equity can be summarized as follows:

- Estimate the firm's future cash flows. Identify the sources and uses of funds, how much money the firm will generate for its providers of capital, and how much liquidity it will need going forward to finance its operating business as well as its investment activities. The financial plan of the firm, which is a core element of the business plan, will provide important answers to these questions. The separate modules Financial Analysis and Financial Planning show how to compile (and understand) a financial plan.

- Assess the riskiness of the firm's future cash flows. Generally speaking, this riskiness is determined by the firm's operating business (i.e., the industry in which it operates) as well as its financing policy (the debt-equity choice). The separate module Cost of Capital shows how to assess these elements and derive the cost of capital.

- Model "Continuing Value." Usually, the cash flow forecasts from (1) cover a limited number of years. The third major step is to think about what might happen with the firm after this explicit forecast period. Will the firm continue to exist? How might cash flows evolve? Etc. The separate module Continuing Value shows how to find answers to these and similar important questions.

- Think about Measurement Error. Each valuation is the result of many assumptions. These assumptions might (and often will) be affected by measurement error. We therefore have to understand what the key value drivers are and how measurement error in these value drivers will affect the valuation result. The chapter Coping with Measurement Error shows how to assess these issues.

The key challenges in startup valuation that we have identified in the indroductory chapter of this module can be traced back to these individual steps. In what follows, we look at some of the major obstacles and present practical ways to tackle these obstacles:

- VAST amount of uncertainty in the business model

- Estimating the risk-adjusted discount rates for TRULY innovative firms

- Incorporating the additional sources of risks many startups have

- How to model continuing values for startups

- Growth in the long run