Reading: Why Go Public?

5. Implications

The preceding sections have shown that the decision to go public can bring massive benefits but often also entails significant costs. We have highlighted the key elements that firms have to navigate when trying to solve this costs-benefits trade-off.

Overall, its looks as if it has become less attractive to be a publicly traded company. The reasons are manyfold:

- After the dot-com "bubble," most exchanges have significantly increased the disclosure requirements, governance standards, and responsibilities of listed firms and their managers (such as the Sarbanes-Oxley Act of 2002). As a consequence, the costs of being listed have increased, and the operational flexibility of listed companies has declined.

- The availability of "cheap" money has opened additional financing sources so that firms do not have to tap into public equity to finance growth. In particular, there was a significant increase in the transaction volumes associated with Venture Capital and Private Equity.

- Together, these could be important reasons why the number of newly listed companies drops (see introduction).

- The dynamics about the operating flexibility of listed firms that we have discussed in the previous section , fueled by the availability of "cheap" money, then also opens new strategic opportunities for listed firms. In particular:

- There is an incredibly active takeover market. In the U.S., about 6% of all listed firms are taken over each year and thereby disappear as legally independent organizations.

- In addition, there is an increasingly active market for going private transactions, in which investors acquire publicly traded companies, often financed with significant amounts of debt (so-called leveraged buyouts, LBOs).

- One of the rationales for this tendency is that, as we have discussed before, it is comparatively more complex to restructure a company under public ownership than when it is privately held. There are too many stakeholders involved and the firm might also have to disclose too much information in the process.

- Therefore, investors first take the companies private and then restructure them under private ownership, possibly to bring (parts of) them back to public ownership at a later stage.

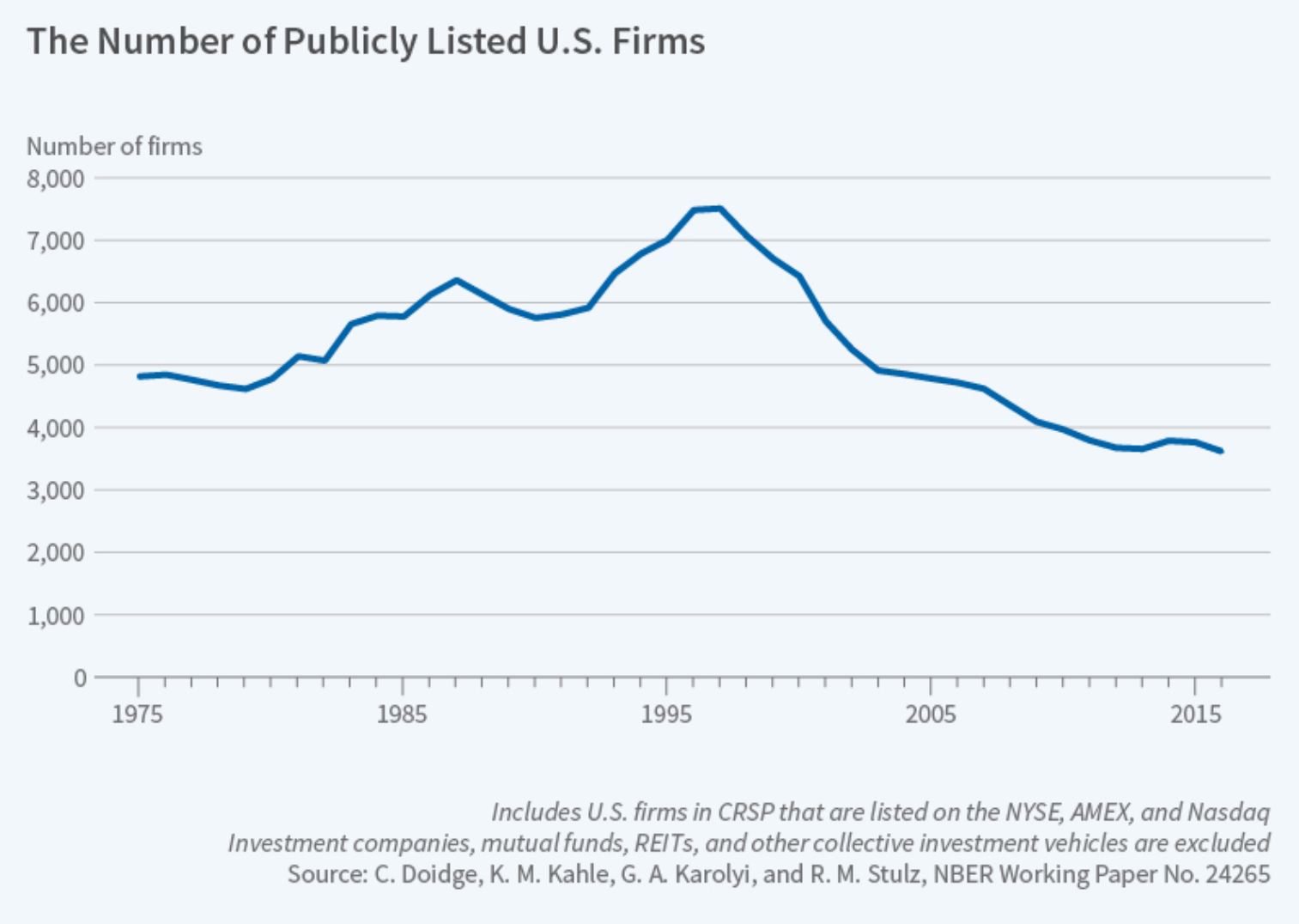

Ultimately, the result of fewer new listings and an active market for delistings (takeover or LBOs) is that the number of listed firms goes down. The following graph, which is from a study by Professor Stulz and co-authors, shows this impressively:

Since the peak of the dot-com era, the number of U.S. listed firms has dropped by almost 50%! And today, there are fewer publicly traded companies in the U.S. than 40 years ago.