Reading: Why Go Public?

2. Listing Strategies and Requirements

There are many competing stock exchanges in the world and the globalization of financial markets has increased the number of options that firms have when deciding about the exchange on which they want to list their securities.

Geographic Location

Basically speaking, firms can choose an exchange in their home country (domestic listing), in a foreign country (cross-border listing), or on several exchanges simultaneously (cross-listing, dual listing):

- Domestic IPO: Facebook's IPO on NASDAQ in 2012 was a domestic IPO, and so was Foxconn Industrial Internet's IPO on the Shanghai Stock Exchange in 2018.

- Cross-border IPO: The Chinese Alibaba Group's IPO on the New York Stock Exchange (NYSE) in 2014 was arguably the most prominent cross-border IPO in history (at least it was the largest).

- Simultaneous IPOs on multiple exchanges are comparatively rarer events. A recent case is Loma Negra Industrial Argentina SA, Argentina's largest cement producer, who raised $800 million in an IPO in Argentina and the New NYSE.

- Cross-listing, in contrast, are comparatively more frequent. These are transactions in which companies who already have their shares listed on a primary exchange list their shares on a different exchange. One of the most prominent examples of a cross listing is the British-Dutch oil and gas company Royal Dutch Shell, which has a primary listing on the London Stock Exchange (LSE) and a secondary listing on Euronext Amsterdam as well as the New York Stock Exchange.

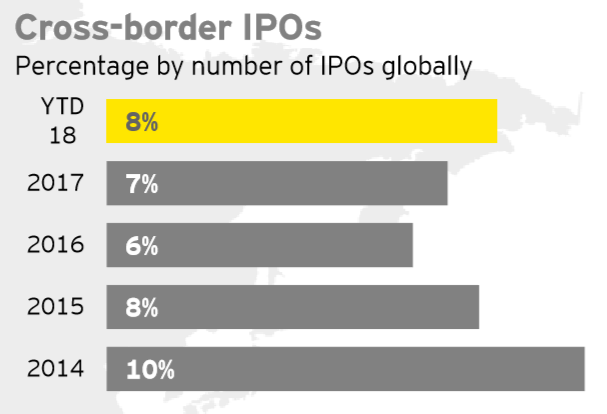

According to EY's IPO survey, the overwhelming majority of all IPOs are domestic IPOs, whereas cross-border IPOs account for less than 10% of the number of transactions, on average:

Choices for Domestic IPOs

Even firms that opt for a domestic IPO often have multiple choices, as some countries have more than one stock exchange and many exchanges have multiple tiers.

For example, in the U.S., the two largest stock exchanges are the New York Stock Exchange (NYSE) and Nasdaq, which originally stood for North American Securities Dealers Automatic Quotation. Nasdaq itself then has three tiers, namely the Nasdaq Global Select Market, which claims to have "the highest initial listing standards of any of the world's stock markets," the Nasdaq Global Market, and the Nasdaq Capital Market, which caters towards smaller and less mature companies.

Similarly, the Deutsche Börse Group offers three market segments, the Official Market with "particularly strict admission criteria and follow-on obligations," the Regulated Market with "slightly less strict admission criteria," and the Open Market that has the lowest admission standards and primarily targets smaller/younger firms.

Listing Requirements

As the preceding discussion suggests, exchanges and exchange segments differ with respect to the specific admission criteria, transparency requirements, follow-on obligations, and admission fees.

While the requirements differ from exchange to exchange, they generally set minimum standards for:

- Size of the company

- Number of publicly held shares

- Minimum value of listed shares

- Liquidity of the listed shares

- Financial viability of the firm

- Financial transparency

- Corporate governance structures and transparency.

For example, the lowest tier of Nasdaq, Nasdaq Capital Market, has the following minimum financial and liquidity requirements (see here for details):

- Nasdaq Capital Market Liquidity Requirements:

- Number of publicly held shares: 1 million publicly held shares (excluding directors, officers, or any person who is the beneficial owner of more than 10% of the total shares outstanding).

- Share price (bid): $4.00

- Number of shareholders: 300 (defined as "round lot holders," i.e., shareholders who own at least 100 shares)

- Number of Market Makers: 3

- Nasdaq Capital Market Financial Requirements: Here, companies can choose between three different standards, the equity standard, market value standard, or net income standard. Under at least one of these standards, they must meet all criteria, as outlined in the following table:

| Requirement | Equity Standard | Market Value Standard | Net Income Standard |

| Stockholders' Equity | $5 million | $4 million | $4 million |

| Market Value of Publicly Held Shares | $15 million | $15 million | $5 million |

| Operating History | 2 years | — | — |

| Market Value of Listed Securities | — | $50 million | — |

| Net Income from Continuing Operations | — | — | $750'000 |

As a comparison, to be eligible for the prime segment, the Nasdaq Global Select Market, firms must have at least 1.25 million publicly held shares (instead of 1 million), 450 round lot shareholders (instead of 300), and a market value of the publicly held shares of at least $45 million (instead of $5 or $15 million). Moreover, they must fulfill at least one of the following financial criteria:

- Earnings standard: Aggregate pre-tax earnings of at least $11 million over the preceding 3 fiscal years

- Capitalization with cash flow standard: Revenues of at least $110 million in the previous fiscal year, aggregate cash flows of at least $27.5 million in the previous 3 years, and an average market capitalization of the listed securities of at least $550 million over the prior 12 months.

- Capitalization with revenue standard: Revenues of at least $90 million in the previous fiscal year and an average market capitalization of at least $850 million over the prior 12 months.

- Assets with equity standard: Total assets of at least $80 million, stockholders' equity of at least $55 million, and a market capitalization of at least $160 million.

Clearly, there are much fewer firms who can potentially meet the latter requirements, which is why a listing on the prime segments of the market is generally marketed by the stock exchanges as prestigious awards of achievement that sends a strong signal of quality and financial strength to investors and other stakeholders of the firm.

Governance and Transparency Requirements

In addition to the financial and liquidity requirements outlined above, firms that go public will often have to make significant changes to their corporate governance structure as well as the communication and disclosure of information. As we will discuss in more details in the sections on the costs and benefits of going (and being) public, these changes can significantly alter the way a firm operates.

In the case of Nasdaq, the governance and transparency requirements are the same across all three tiers. In particular (see here for a full list of governance requirements):

- Firms must make their annual and interim reports publicly available. Privately held firms generally have no obligation to disclose financial information.

- The accounting standards have to follow international rules (US GAAP or IFRS) and the firm must provide an audit track record of at least three years.

- The majority of the members of the board of directors must be independent directors.

- The firm must have an audit committee that solely consists of independent directors "who can read and understand fundamental financial statements."

- The firm must also have a compensation committee that solely consists of independent directors. This committee determines (or recommends) the compensation of all executive officers.

- Nominees for directors must be selected or recommended by independent directors.

- The company must adopt a code of conduct.

The purpose of this section was to provide a rough overview of what it takes for companies to be eligible for public listing. It is clear that most companies will never meet the financial requirements to be eligible for listing. Moreover, it is conceivable that many companies that do meet the requirements will not want to list because of the fundamental changes in the governance and transparency that such a decision brings about.

For the interested reader, the following report by PWC provides a more detailed comparison of the of the specific regulatory listing requirements on five major stock markets, namely:

- London Stock Exchange (LSE)

- Hong Kong Stock Exchange (HKEx)

- New York Stock Exchange (NYSE)

- NASDAQ

- Singapore Exchange (SGX)