Reading: The Going Public Process

3. Due Diligence and Regulatory Filings

The next important step is to get the firm ready for the IPO, especially from an accounting, compliance, and regulatory point of view.

Publicly traded companies are subject to much stricter disclosure and accounting standards than most privately firms. An IPO therefore usually implies a significant change in how the firm the firm prepares and presents its financial information. To cope with these complexities, the issuing firm often relies on external auditors and financial reporting expert. It also hires legal experts to help navigate the securities law and provide legal due diligence. As we have seen in the overview of the costs of going public, the associated accounting and legal costs are usually the largest cost block besides the underwriting discount.

At the same time, the underwriter has to draft a set of documents for the registration of the shares. Below, we provide a rough overview of the most important documents as well as their key elements, namely:

A) Engagement Letter

B) Letter of Intent

C) Red Herring Prospectus

D) Underwriting Agreement and Final Prospectus

A) Engagement Letter

The first document is an engagement letter that outlines the financial compensation of the underwriter. It usually contains two main elements, namely the underwriting discount (gross spread) as well as a reimbursement clause:

- Underwriting discount: The discount at which the the underwriter can purchase the securities from the issuer.

- As we have discussed in the section on the costs of going public, the underwriting discount generally corresponds to 4% to 7% of the price at which the shares are sold to the investing public on the primary market.

- This underwriting discount is the main source of income for the syndicate; and it is what makes an IPO substantially more expensive than other forms of going public.

- In the case of Dropbox, the underwriting discount was set to 4.45% of the gross proceeds.

- Reimbursement clause: A standard clause that states that the issuing firm must cover all of the underwriter's out-of-pocket expenses. This clause also applies if the firm withdraws its IPO at any later stage.

B) Letter of Intent

The parties also prepare and sign a letter of intent, which summarizes the preliminary understanding of the proposed deal. Formally,

- the underwriter commits to enter into an underwriting agreement with the issuing firm,

- and the issuing firm commits to disclose all relevant information to the underwriter and to fully cooperate in the due diligence efforts.

The letter of intent also summarizes the main characteristics of the planned offering. In particular:

- Underwriting arrangement: Firm commitment or best effort

- There are two basic ways how the investment bank can broker the issuing firm's shares to the investing public: via firm commitment or best efforts arrangement.

- With a firm commitment, the underwriter commits to purchase the whole offer (which will be defined in the underwriting agreement) from the issuing firm.

- The issuing firm therefore knows exactly how much money it will raise in the IPO. It is then the underwriter's responsibility to place the shares with the investing public.

- The overwhelming majority of all IPOs is conducted via firm commitment.

- Alternatively, the parties can enter into a best efforts agreement, under which the issuer receives no guarantee from the underwriter with respect to the amount of capital that will be raised.

- With such a best efforts agreement, the underwriter simply sells securities on behalf of the issuing firm.

- Deal size: The letter of intent also indicates the potential size of the transaction, possibly including valuation ranges of the securities to be sold as well as the amount of capital to be raised.

- Greenshoe option: Finally, the letter of intent usually also includes a so-called greenshoe or overallotment option, according to which the underwriter receives the right buy up to an additional 15% of the company's shares at the offering price (net of underwriting discount). As we discuss later, this greenshoe option facilitates the underwriter's efforts to stabilize trading after the IPO.

- Importantly, the letter of intent does not contain a final price for the offering, as this price first has to be determined in the marketing and pricing of the transaction.

C) Registration Statement (Red Herring Prospectus)

After signing the letter of intent, the company, with the support of the underwriter and external experts, will begin the long and cumbersome process of drafting the registration statement, which is known in the United states as the Form S-1 Registration Statement Under the Securities Act of 1933. The preceding link contains a template of that form. Form S-1 consists of two main parts, namely the IPO prospectus as well as additional private filings:

Part 1: IPO Prospectus

- The Prospectus is a legal document

- It contains detailed information about the companies business plan, the competitive landscape, how the firm plans to use the proceeds from the offering, and what the risk factors are. Moreover, it discloses information about executive compensation, the audited financial statements, the number of securities sold, the amount being sold by individual shareholders, etc.

- The prospectus is made available to every investor who buys the security.

Part 2

- The second part of Form S-1 covers information that is not legally required in the prospectus, such as recent sales of unregistered shares and additional exhibits.

- This information is provided to the SEC to support the SEC's due diligence efforts. It is not necessarily made publicly available.

The purpose of the registration statement is to ensure that investors have sufficient and reliable information about the issuing firm. Since it is a legal document, the issuer will be liable for material misrepresentations or omissions.

The filing of the registration form marks the official application of the firm to go public and the start of the financial market authorities' due diligence process. Moreover, the filing date is, in most instances, when the public learns about the firm's intention to list its shares on a public exchange.

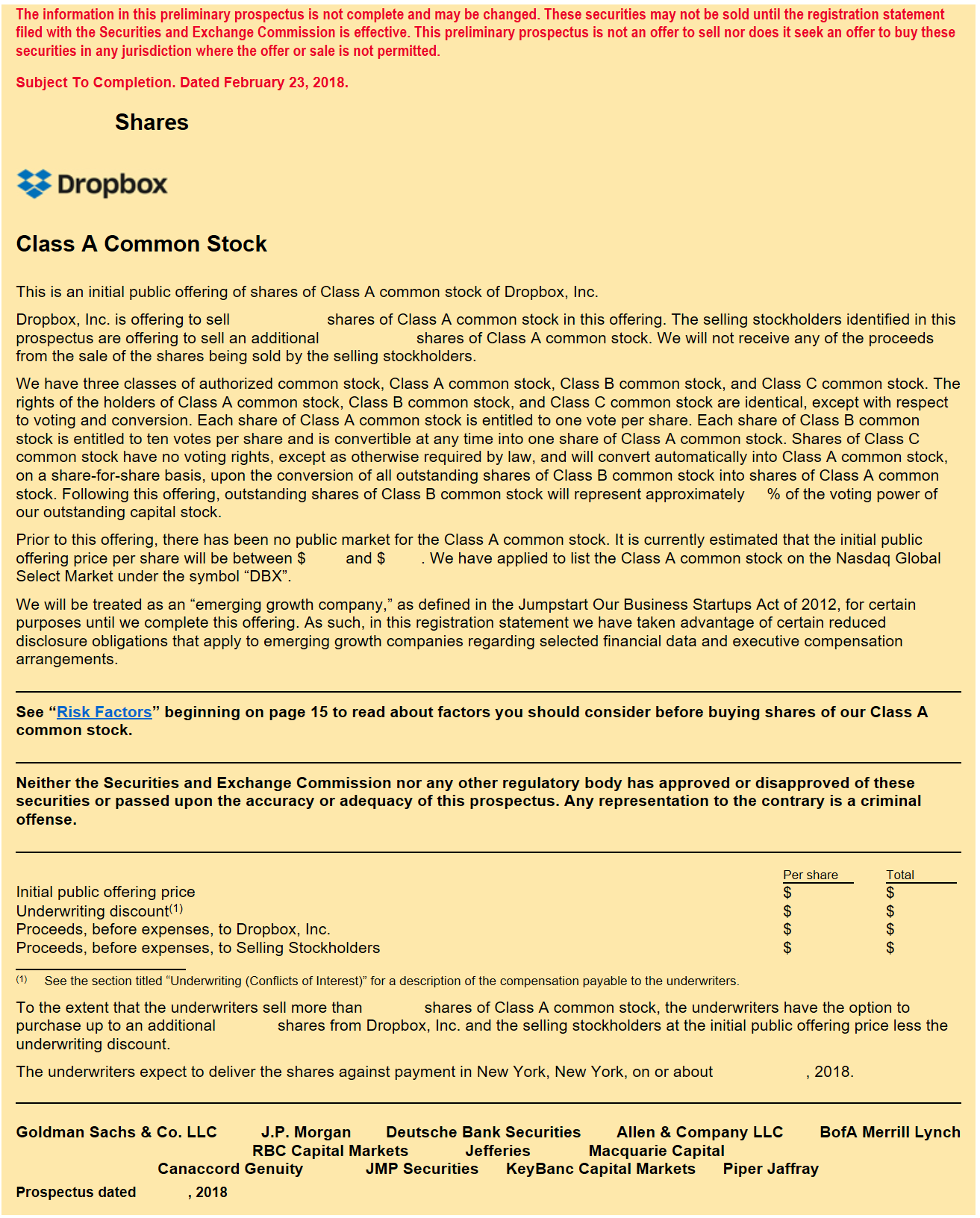

Dropbox filed its preliminary Form S-1 registration statement on February 23, 2018. As not all relevant information of the transaction is available at the time of the original filing, the preliminary prospectus is incomplete. Most importantly, at the time of initial filing, the firm generally does not know the exact number of shares to be sold nor the issue price of the shares and the amount of issue. These items will need to be determined during the marketing and pricing phase of the issue.

Because of its preliminary nature, the cover page of the document displays a bold red disclaimer that the information in the document is incomplete and may be changed. This red disclosure statement is also why the initial filing is generally referred to as Red Herring Prospectus. It is also nicely visible on the front page of Dropbox's original filing (click page to enlarge):

D) Underwriting Agreement and Final Prospectus

During the marketing and pricing phase of the IPO, the previously discussed letter of intent remains the governing document of the relationship between the issuer and the underwriter(s).

Once the IPO is approved by the SEC, the so-called Effective Date is determined. This marks the date at which shares can first be traded on the stock exchange. The earliest possible effective date is 20 days after the registration filing. During this so-called cooling-off or waiting period, the SEC conducts its due diligence and communication between the firm and the (potential) investors is greatly restricted.

Finally, on the day before the effective date, the underwriter and the issuing firm decide on the initial offer price and the exact number of shares to be sold.

The details about the pricing and the allocation of shares among the underwriting syndicate are summarized in the underwriting agreement between the issuer and the underwriter. With the underwriting agreement, the underwriter is legally bound to purchase the specified number of shares at the specified price from the issuer.

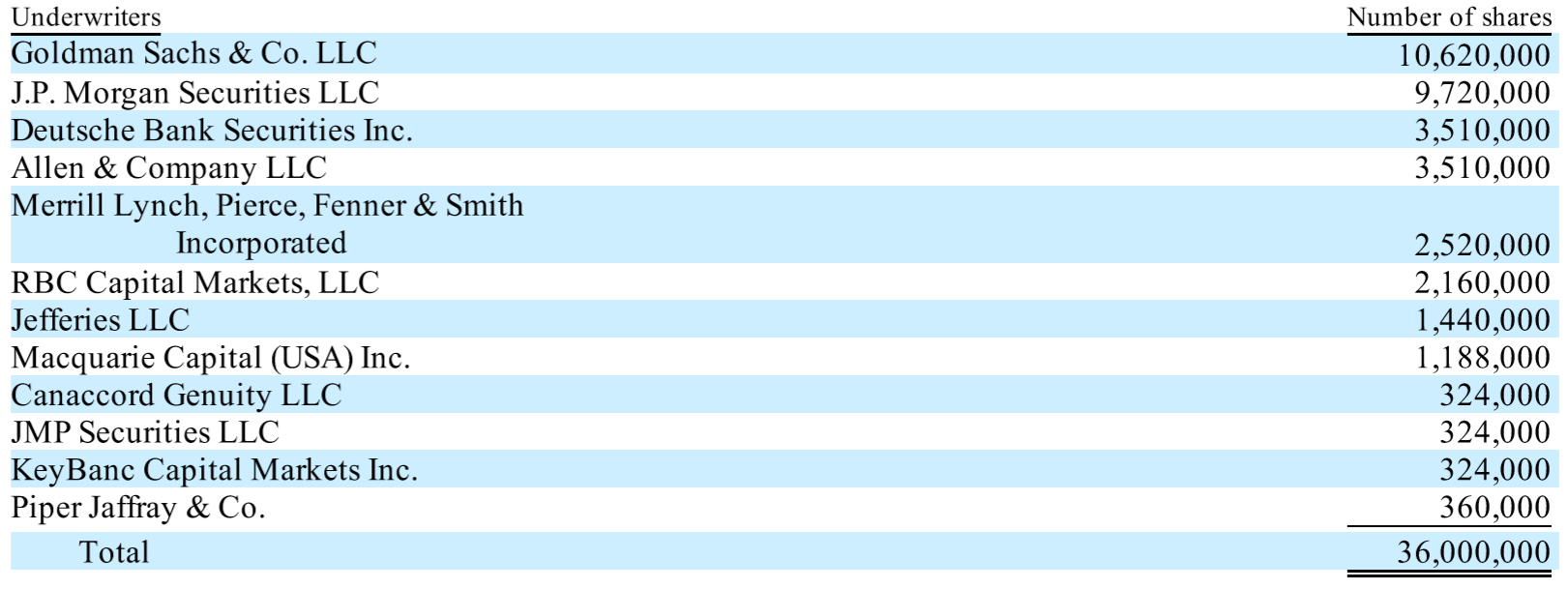

For example, in the case of Dropbox, Goldman Sachs has agreed to underwrite approximately 10.6 million shares, J.P. Morgan Chase has underwritten 9.7 million shares, and the remaining approximately 15.7 million shares were underwritten by the ten other members of the syndicate, as shown in the final listing prospectus:

Once the SEC determines that all relevant information is disclosed in the registration statement, the company disseminates its final prospectus. In the case of Dropbox, the firm filed its final prospectus on March 22, 2018, the day before the shares started trading on NASDAQ. The sheer length of the document—240 pages—is prove of how complex and time-consuming the formal preparation for the IPO is.