Reading: IPO Mechanics

7. Extensions

7.1. Who Pays the Underpricing?

In the preceding example, we have seen that the IPO that we have considered is underpriced by $55.65 million, meaning that the total value of shares offered to the primary investors exceeds the price these investors pay by that amount.

Who pays the difference? The answer is very simple: The original shareholders.

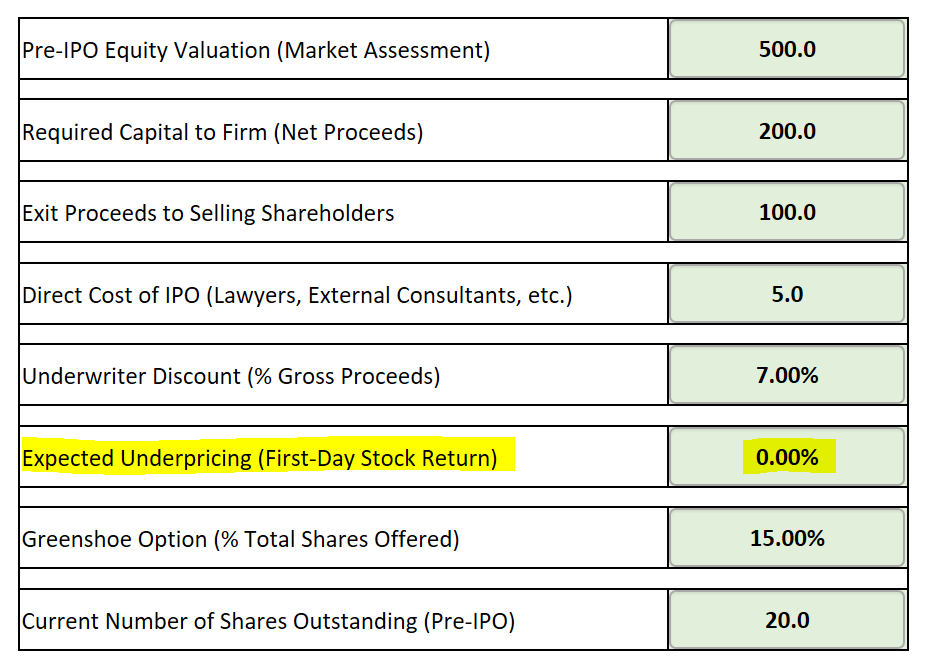

We can see this when we set the assumption of underpricing from 15% to 0% in the Online Tool:

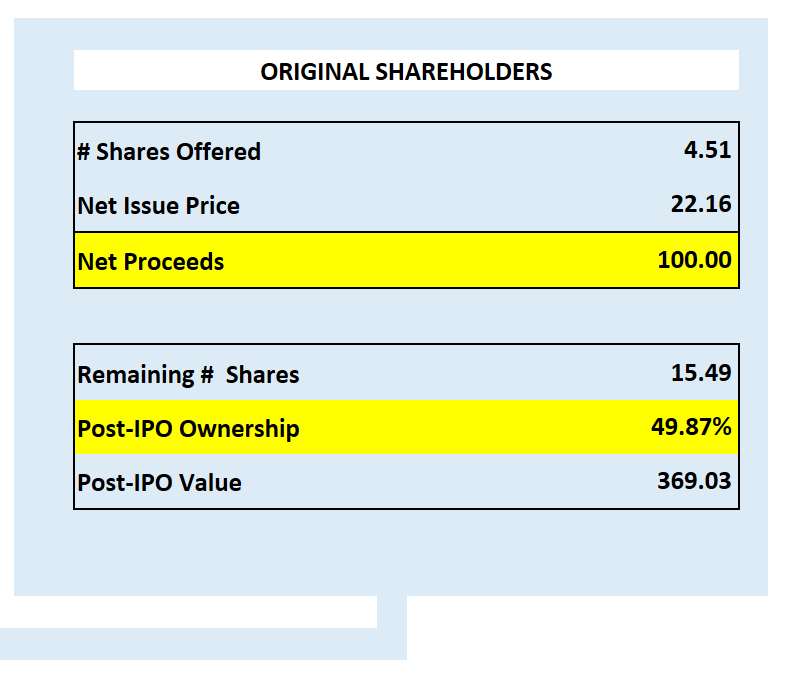

The transaction summary on the last tab of the tool then shows that under these revised assumptions, the post-IPO value that goes to the original shareholder is indeed $55.65 million higher, namely $369.03 million instead of 313.39 million:

This is important to remember. Underpricing is not any type of unaccounted value that magically arises during the IPO process. It is ultimately paid by the original shareholders to get access to the primary investors and the subsequent stock market listing.