4. Readings: Future Values with Multiple Cash Flows

2. Multiple Cash Inflows

Many investment proposals involve more than just one initial cash flow. For example, think of an investor who wants to put aside a certain amount of money each year to save for old age. This investor will be interested to know how much money she can expect to have in her account at the time of retirement.

Example 1:

An investor puts aside USD 100'000 today and another USD 100'000 in 2 years. How much money will the investor have in the bank account 4 years from now if she earns an annual interest rate of 5% (payable at the end of the year)?

There are two ways to solve this problem, namely:

- Model the year-to-year development of the account

- Compute the sum of the future value of each individual cash flow.

In what follows, we take a closer look at the two approaches to compute the future value of the investment proposal in question.

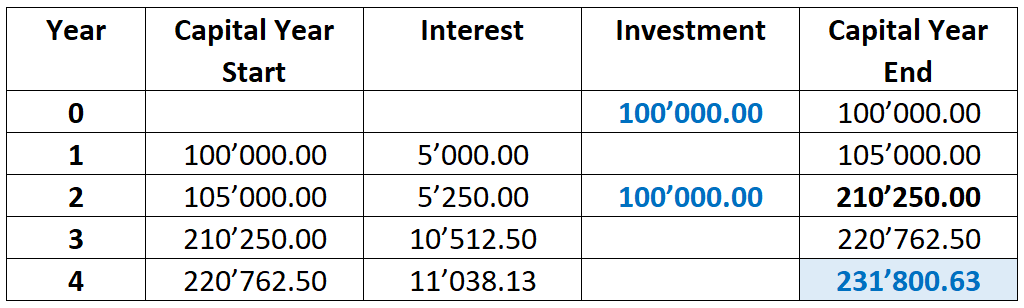

Modeling the Account Balance

The following table models the year-to-year development of the account that is associated with the investment proposal in question. The computations are also summarized in the accompanying Excel file.

Here is what the table shows:

- Each row of the table shows the relevant events during one year of the investment period.

- The project starts with an investment of 100'000 today. "Today" refers to the beginning of year 1, which is equivalent to the end of year 0.

- The investment then earns a return of 5% at the end of year 1 and 2, respectively. Therefore, the corresponding interest payments are:

- USD 5'000 in 1 year [= 100'000 × 0.05], so that the balance increases to USD 105'000,

- USD 5'250 in 2 years [= 105'000 × 0.05], so that the balance increases to USD 110'250.

- By the end of the second year, the initial investment will therefore grow to USD 110'250. At that time, the investor also makes the second payment of 100'000, so that the overall balance increases to USD 210'250 [= 110'250 + 100'000].

- For the remaining 2 years, the investor then earns interest on that amount, namely:

- USD 10'512.5 [= 210'250 × 0.05] at the end of year 3, so that the balance increases to USD 220'762.5

- USD 11'038.13 [= 220'762.5 × 0.05] at the end of year 4, so that the balance increases to USD 231'800.63.

- Consequently, by the end of year 4, the investment proposal will yield a future value of USD 231'800.63.

Future Values of Individual Cash Flows

Alternatively, we can look at the two investments of USD 100'000 separately and compute their respective future values in 4 year:

-

Today's investment of 100'000 (C0) will earn interest of 5% over 4 years. Consequently, it's future value in 4 years is:

\( FV_{C_0,4} = 100'000 \times 1.05^4 = 121'550.63 \)

- In contrast, the second investment of 100'000 in 2 years (C2) will only earn interest over two remaining years, namely at the end of year 3 and the end of year 4, respectively. Consequently, it's future value is:

\( FV_{C_2,4} = 100'000 \times 1.05^2 = 110'250.00 \)

In 4 years, the investor will therefore have USD 231'800.63, namely USD 121'550.63 from the first investment plus USD 110'250.00 from the second investment. This is the same future value as we have computed before.

The example might be simple, but it conveys a very important message, the so-called Principle of Value Additivity: The future value of a string of cash flows can be calculated as the sum of the future value of each individual cash flow. This principle holds as long as we compute the future value of each cash flow for the same future point in time (in our example 4 years from now).

In our example, we can therefore compute the future value of the investment proposal as follows:

\( FV_4 = C_0 \times (1+R)^T + C_2 \times (1+R)^{(T-2)} \)

\(FV_4 = 100'000 \times 1.04^4 + 100'000 \times 1.04^2 \)

\( FV_4=121'550.63+110'250.00=231'800.63 \)

As we have seen already several times, the general expression to compute the future value at time T of a cash flow at time t is:

\( \bf{FV_T = C_t \times (1+R)^{(T-t)}} \)

Similarly, the future value of a string of cash flows between time 0 and time T can be computed as:

\( \bf{FV_T=C_0 (1+R)^T + C_1 (1+R)^{T-1} + C_2 (1+R)^{T-2}+...+C_T}\)

Using the symbol \( \sum \) to denote the sum of a series of arguments, this latter expression can be written as:

\( \bf{FV_T = \sum_{t=0}^{T} C_t \times (1+R)^{(T-t)}} \)