Reading: Implementing Real Option Valuation

3. Case Applications

3.1. Option to Delay

An option to delay means that the holder has the exclusive right to a specific investment decision for a predefined period of time. The holder can take that decision today or he can delay it to a later date.

When we conduct a standard DCF valuation, we obtain the value of the investment decision if we take it today (or at any given future point in time). It does not really tell us, however, whether it could be more valuable to postpone the decision to a future date.

The classic example of an option to delay is a patent. A patent provides the owner of the patent with the right to develop and market a specific product.

A rational decision maker will only make the necessary investments (X) to develop and market the product in question if the value of the expected future earnings (S) exceeds the investments (S>X). If not, the firm can hold on to the patent and postpone the decision.

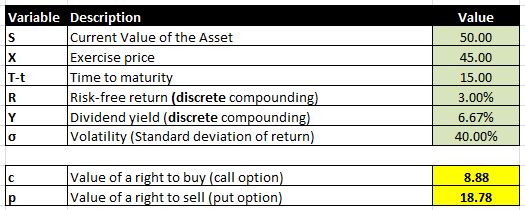

Example:

Suppose a pharmaceutical company has a patent on a new approach to treat cancer. The firm came up with the following information:

- A DCF valuation as of today implies that the present value of all future cash flows that are associated with the drug is 50 million

- A simulation of different DCF valuation scenarios also implies that the volatility of the value estimate is 40%

- The cost of developing the drug is 45 million

- The patent lasts 15 years

- The risk-free rate of return is 3% (discrete compounding)

- After the patent expires, competitors will be able to perfectly replicate the drug so that the NPV of the investment project will be 0. Therefore, we assume that the cost of delay (y) equals 1/15, that is, that for each year we postpone the project, we lose a year of value-creating cash flows)

Based on this information, we can value the patent as a call option on the underlying drug. If we plug the 6 valuation parameters in the Black-Scholes-Merton model, we find (in millions):

Therefore, based on our assumptions, the value of the patent on the drug is 8.88 million.

Note that the intrinsic value of the option (the value if we exercised the option today) is only 5 million:

Intrinsic value = S - X = 50 - 45 = 5 million.

Consequently, it is more valuable to postpone the investment decision (8.88 vs. 5 million).

How confident can we be about this valuation? Let's do the real option test from before:

1. Is there a real option embedded?

- The answer would seem to be yes.

- There is an underlying asset - the product generated by the patent; the firm has the right to exploit this investment opportunity; and the relevant contingencies are also "clear:" Develop the product if S > X.

2. Is there exclusivity?

- This question is a bit trickier. The initial answer would be yes, too. After all, the patent grants the firm exclusivity to produce the product that is protected by the patent. In this sense, the patent eliminates competition.

- But that does not mean that the firm has exclusivity for the underlying market! Other firms might find different treatments for the same disease!

- So exclusivity would seem to be limited, even with a patent!

3. Can we use option pricing models?

- Neither the underlying asset (market for cancer cure) nor the option (patent) are traded. So it will be almost impossible to build a replicating portfolio.

- There is a market for individual patents, but it is rather illiquid

- Mature companies should at least be able to roughly quantify the costs associated with development and market entry.

In sum, there clearly is an option, but the quality of the valuation will be a direct result of the quality of the initial capital budgeting exercise to determine the current value (S) as well as the volatility (σ).