Reading: Implementing Real Option Valuation

3. Case Applications

3.3. Option to Abandon

Finally, firms often have the option to stop a project (or at least scale it down) if the actual cash flows fall short of the initial expectations. In a sense, this offers the firms some loss protection. By limiting the downside risk, the overall project becomes more valuable.

We have already encountered several abandonment options:

- An oil company that can stop the project if they do not find oil

- A pharmaceutical company that can stop the project before investing into production facilities if its drug does not receive FDA approval.

- etc.

Example (Damodaran, p. 236):

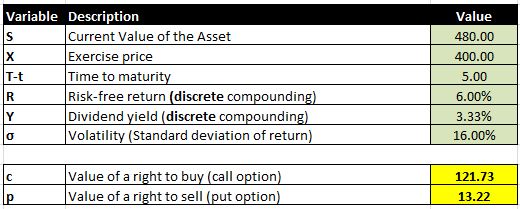

Suppose Airbus considers a joint venture with Lear Aircraft for a small commercial jet. The plan is for Airbus to invest 500 million in exchange for 50% of the joint venture. According to a current DCF valution of the project, a 50% stake in the joint venture has a value of 480 million today.

Lear Aircraft loves the project and is absolutely convinced that it will work out. To convince Airbus to join in the venture, it offers Arbus to buy back its 50% share anytime over the next five years for 400 million if Airbus wants to get out.

The simulations of the DCF analysis have produces a volatility of the underlying value of 16%. The project has an expected lifespan of 30 years and the risk-free rate of return is 6%.

What shall Airbus do?

The first immediate conclusion is that Airbus should not invest without the option to abandon, since the 50% ownership stake is less valuable than the required investment:

NPV Joint Venture without option = - Investment + Value of ownership stake = -500 + 480 = -20 million.

So the question is whether the abandonment option can turn that negative value into a positive one. To find out, we have to value it. The relevant parameters are:

A few points are worth noting:

- The time to maturity of the option is 5 years. While the project lasts 30 years, Airbus can only sell back to Lear Aircraft within the first 5 years.

- If the lifespan of the project is limited to 30 years, the value of the project will gradually erode to 0 over the 30 years. We can incorporate this (roughly) by setting the dividend yield to 1/30 = 3.33%.

Based on our analysis, the right to sell the joint venture stake back to Lear Aircraft has a value of 13.22 million today. Consequently, the value of that option is not sufficient to turn the negative NPV positive. The overall value of the project is -7 million:

NPV Joint venture = Value joint venture + Abandonment option = -20 + 13 = -7 million.

Even thought the NPV is negative, it still makes sense to look at the real option test.

1. Is there a real option embedded?

- The answer would seem to be yes.

- There is an underlying asset - the jet project; the firm has the right to sell its share in the jet project to Lear Earcraft; and the relevant contingencies are also "clear:" sell if if S < X.

2. Is there exclusivity?

- Yes, there is exclusivity, since the right to sell is contractually granted.

- The question is, however, how valuable that exclusivity is. Put differently, will Airbus be able to enforce it? Once concern could be that the right becomes valuable only if the project is a flop. In this situation, the financial health of Lear Aircraft might not suffice to pay the 400 million to Airbus!

3. Can we use option pricing models?

- Neither the underlying asset (soft drings) nor the option (expand production) are traded. So we will need our own valuation to assess S and σ.

- There is no uncertainty about the exercise price.

In sum, there is a real option embedded in the project but it is not clear how valuable it is, given that exclusivity might be limited. Moreover, there are a few challenges to estimate the valuation parameters. Consequently, the result of the valuation will be noisy and we risk overestimating the value of the project as a whole.